In my last post, I talked about how a structured 5-day gym routine builds the professional muscle you need to survive audit season. But as any seasoned athlete knows — strength alone doesn’t win matches. You need a game plan.

A bold one.

Last week, I promised to explain why tax planning is exactly like a T20 run chase. But then the 2026 T20 World Cup happened — and India tore up that script entirely.

They didn’t win by nervously watching the scoreboard and chasing down a target in the final over. They batted first. They walked out, took guard, and set a target so commanding that the opposition never felt in the game. Dominant, proactive, and dictating the pace from ball one.

That is precisely what the Finance Bill, 2026 has done for domestic manufacturers stuck in an Inverted Duty Structure. For the first time, you are no longer chasing your own refund. The government is handing you the opening bat.

The Liquidity Chase: A Problem Every Manufacturer Knows Too Well

If your business operates under an Inverted Duty Structure (IDS) — where you pay GST at 18% on your raw materials but can only charge 5% on your finished goods — you already know what I call the “Liquidity Chase.”

Your Input Tax Credit (ITC) keeps accumulating. You file for a refund. And then you wait. And wait. Weeks blur into months. Your working capital is locked inside a government queue while your suppliers, your payroll, and your expansion plans all sit on hold.

Until now, the rules were deeply lopsided — and honestly, a little unfair:

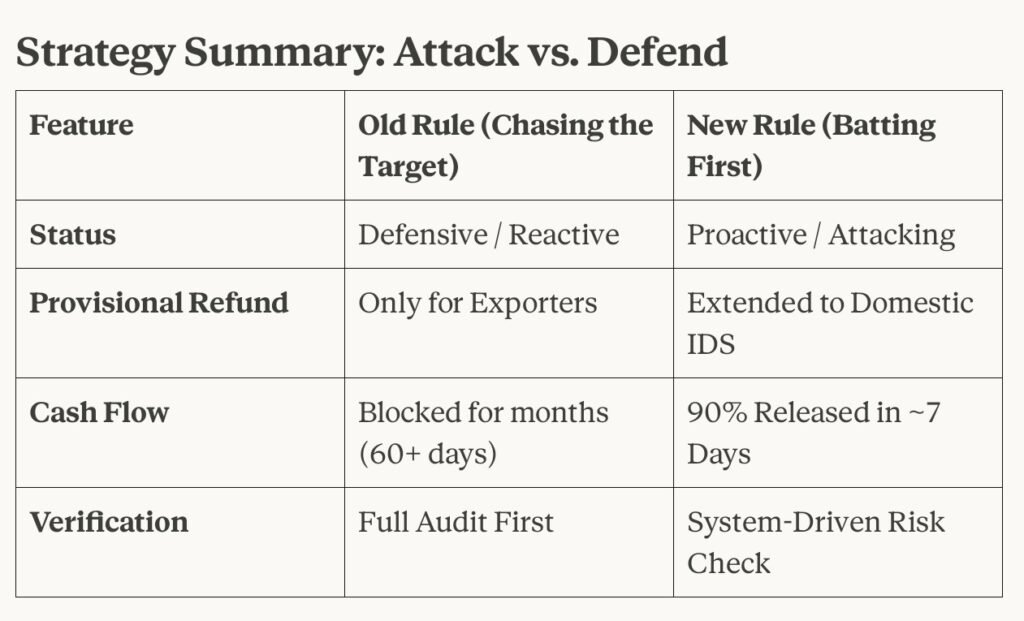

Exporters enjoyed a clear Powerplay advantage. Under the existing Section 54(6) of the CGST Act, they were eligible for a provisional refund of 90% of their claim — released rapidly, before any formal audit was completed.

Domestic Manufacturers under IDS? They were forced to play the long game. Every rupee of their refund was held back until a full manual audit was done. No fast track. No provisional release. Just patience — and blocked cash flow.

If you have ever wondered why exporters seemed to get better treatment under GST than domestic businesses, this was the specific provision that created that disparity.

The Strategy Shift: Clause 139 Changes Everything

Clause 139 of the Finance Bill 2026 (refer to page 218 of the finance bill for clause 139) proposes to amend Section 54(6) of the CGST Act to officially extend the 90% provisional refund facility to IDS refund claims. While some of you may have already tasted this speed through administrative workarounds or pilot programmes that quietly ran late last year. But here is the crucial distinction — those were workarounds. Clause 139 is the legislative full stop. It enshrines this right permanently into the Statute, stripping away every last grey area and leaving no room for ambiguity going forward.

Read that again. Because it is significant.

The government is no longer asking domestic manufacturers to wait for the full “death overs” audit before releasing funds. Instead, 90% of your legitimate IDS refund claim will be released within approximately 7 days of acknowledgment — based on automated, system-driven risk checks — while the remaining 10% continues through formal scrutiny.

This is not just a procedural tweak. This is a fundamental philosophical shift in how the government approaches GST refunds — from an era of suspicion and paperwork to one of trust-based, technology-first compliance. You set the target. The audit follows.

Who Hits a Six with This Amendment?

While this reform benefits any registered taxpayer with an accumulated ITC refund under an IDS, certain sectors are the undisputed Heavy Hitters of this policy change:

Textile Manufacturers — Raw fibres and yarn attract higher GST rates, while finished fabrics and garments are taxed lower. The inverted structure here is chronic, and refund delays have long squeezed liquidity across the supply chain.

Chemical and Fertilizer Units — High-taxed raw chemicals feed into end products that attract lower rates, creating a persistent IDS trap. These businesses will now see their working capital freed up significantly faster.

Pharmaceutical Companies — Active Pharmaceutical Ingredients (APIs) often attract higher GST than the life-saving medicines manufactured from them. For mid-sized pharma manufacturers especially, this 90% provisional release could be transformational.

By unlocking the majority of the refund claim almost immediately, the government is effectively eliminating the “junk volume” of waiting time — freeing you to reinvest in raw material procurement, production capacity, or debt reduction without breaking your cash cycle.

The Tax-Athlete Connection: Batting First Is a Mindset

Here is where I want to pause from the legal analysis, because this amendment is more than just a policy update. It reflects a mental framework that I genuinely believe in — both in tax and in training.

In the gym, a reactive athlete always plays catch-up. They train only when they feel like it, respond to soreness instead of preventing it, and wonder why their progress plateaus. A proactive athlete builds the programme first, controls the variables, and lets the results follow the structure.

In business, the same truth applies. For years, domestic manufacturers were reactive by design — the law forced them into a defensive crouch, chasing refunds and protecting cash flow instead of deploying it. This amendment puts them on the front foot. It lets you plan your quarterly cash flows with confidence, knowing that 90% of your legitimate ITC refund is not stuck in bureaucratic limbo.

Batting first in cricket is a statement of intent. This amendment, in its own quiet way, is the government making the same statement to India’s domestic manufacturing sector.

Your Pre-Match Checklist: Don’t Get “Run Out” at the Non-Striker’s End

In a high-stakes T20, a single avoidable run-out can completely shift momentum. In GST refunds, a small data mismatch or a missed compliance condition can have the exact same effect — your claim gets flagged as “High Risk” and the 90% fast-track payout is blocked.

Before you file your RFD-01, make sure your fielding is watertight:

GSTR-2B Synchronization: Every rupee of ITC you are claiming must reconcile 100% with your auto-populated GSTR-2B. Even a small discrepancy triggers a High-Risk flag and stops the provisional release cold.

Statement 1A Validation: This system-computed statement is the mathematical heart of your IDS refund calculation. Verify it carefully — an error here is the difference between a boundary and losing your wicket.

The Clean Record Check: Under Rule 91, your business must not have faced prosecution for tax evasion exceeding ₹2.5 crore in the preceding 5 years. If there is any such exposure, the provisional route is unavailable to you.

Rule 89(4B) Compliance — Inputs Only: The 90% fast-track applies exclusively to ITC on inputs (raw materials). Do not accidentally include ITC on capital goods or input services in your IDS formula, or your calculation will be rejected.

Aadhaar Authentication (Rule 10B): Your Aadhaar-based authentication must be completed. If this step is pending, the provisional refund is blocked regardless of how clean your filing is.

PFMS Bank Account Validation: Your linked bank account must be validated through the Public Financial Management System. A sanctioned refund that cannot be disbursed due to a bank validation error is one of the most frustrating — and entirely avoidable — outcomes in GST compliance.Treat this checklist the way a cricketer checks his kit before a match. The preparation before the game determines how well you perform in it.

The Bottom Line: Own the Powerplay

Getting your 90% refund provisionally is the equivalent of winning the toss on a flat pitch, choosing to bat, and putting 60 runs on the board in the Powerplay. It gives you early momentum, strategic flexibility, and psychological control over your business planning.

But — and this is important — the remaining 10% still goes through full scrutiny in the “death overs.” Your documentation needs to be in order. Your filings need to be clean. The government has extended trust; your job is to honour it with meticulous compliance.

Consistency in the gym builds physical strength. Consistency in GST compliance builds the kind of professional authority that no notice, no audit, and no tax officer can shake.

Stay on the front foot. File clean. Bat first.

Next week, we move from the cricket pitch to the global arena — because sometimes the biggest threat to your business isn’t inside your GST portal, it’s 1,500 miles away in open water. See you then.

Disclaimer: This blog post is for informational and educational purposes only and does not constitute professional tax, legal, or financial advice. The provisions of the Finance Bill, 2026 are subject to final parliamentary approval, presidential assent, and official government notification. Always consult a qualified tax professional regarding the specific application of these laws to your business circumstances.