The Warm-Up: Where We Left Off

Last week, I broke down how GST 2.0 restructures India’s entire rate architecture, collapsing four slabs into three and clearing out classification disputes that have kept tax professionals busy for years. Before that, we covered why domestic manufacturers can finally stop chasing their own refunds under Finance Bill 2026. Both those posts looked at structural changes to the system itself. Today, that same framework gets pointed at something most people treat as pure entertainment. The IPL is India’s most-watched commercial spectacle and, from a tax perspective, one of its most instructive indirect tax case studies.

The 60-Second Version

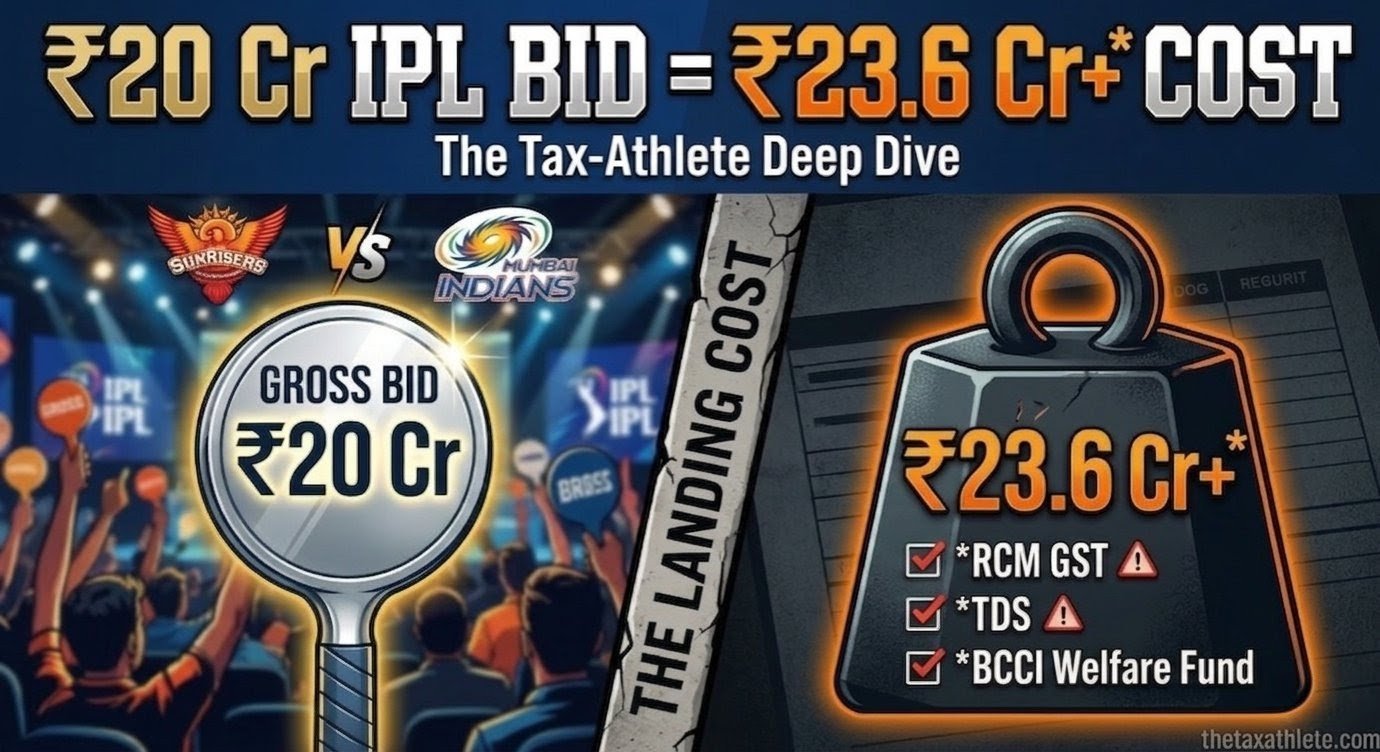

- A ₹20 crore auction bid is not the franchise’s final cost. Between TDS, GST and the BCCI welfare fund, the actual cash outlay can reach ₹23.6 crore or more

- Indian players: 10% TDS under Section 194J and 18% GST under RCM, paid in cash by the franchise upfront

- Overseas players: 20% withholding tax under Section 115BBA and 18% GST under RCM, also in cash, no deferral

- The Impact Player earns the auction contract amount plus a match fee of ₹7.5 lakhs per match, both taxed separately

- Benched players still receive their full auction contract. Only the match fee requires actual playing participation

- Injury insurance runs in two layers. BCCI covers national-duty injuries; franchises hold their own policies for IPL season injuries. Compensation payouts carry no GST liability

- The BCCI’s 2026 mini-auction rule caps overseas player earnings at ₹18 crore. Any excess bid goes to the Player Welfare Fund, not the player

- IPL tickets now attract 40% GST under GST 2.0, classified as luxury entertainment alongside casinos

- RCB sold for $1.78 billion in March 2026, the highest franchise valuation in cricket history

The auctioneer scans the room. Kavya Maran raises the Sunrisers Hyderabad orange paddle. Across the aisle, Mumbai Indians counter without hesitation. The number on the board climbs. The crowd watching the live stream reacts in real time. And back at the franchise office, a CFO is already running a different calculation entirely, one that has nothing to do with the number on that screen.

That gap between what the scoreboard shows and what the balance sheet records is what this post is about. The bid price is the sticker. The landing cost is a different number altogether. Let us go through what that number actually looks like, and why the taxman always bowls the first over.

1. Two Taxes, One Transaction: How a Player Gets Paid

The first thing that surprises most people is that a player’s paycheck appears to be taxed twice. It is not double-dipping. It is the legal distinction between two entirely separate levies operating on the same transaction at the same time. One is a tax on income. The other is a tax on the supply of a professional service. Both are real. The franchise handles both.

The Indian Player: Section 194J TDS + 18% GST Under RCM

Under the Income Tax Act, an IPL player is classified as an Independent Professional, not a salaried employee. The franchise does not put them on a payroll. The player raises an invoice for their services and the franchise withholds 10% TDS on the contract value under Section 194J of the Income Tax Act, 1961, before paying out the balance. That TDS reaches the government as the player’s advance income tax.

Here is the part most people do not expect. Under Section 9(3) of the CGST Act, 2017 read with Notification No. 13/2017-CT(Rate), when an individual sportsperson provides services to a body corporate, which is exactly what an IPL player does when they suit up for a franchise, the franchise is liable to pay GST under Reverse Charge Mechanism (RCM). The player does not charge GST on their invoice. The franchise pays 18% directly to the government in cash. For most business transactions, GST is charged, collected and then claimed back as Input Tax Credit (ITC). Under RCM, the franchise pays first and claims the ITC only in a later return period. The cash goes out before the credit comes back.

The Overseas Player: Section 115BBA + 18% GST Under RCM

For international players, the structure tightens further. Under Section 115BBA of the Income Tax Act, 1961, foreign sportsmen earning in India are taxed at a flat 20% on gross income plus applicable surcharge and cess. No deductions. No exemptions. A straight 20% hit on the gross contract value, withheld by the franchise before payment.

The GST treatment is identical: 18% under RCM, paid in cash by the franchise. While the withholding tax rate is higher for an overseas player, it remains a deduction from the bid price, meaning the franchise’s total cash commitment stays exactly the same as it would for an Indian player.

2. The Impact Player and the Benched Player: Two Very Different Ledgers

The Impact Player: A Match Fee on Top of the Contract

The Impact Player rule, introduced in IPL 2023 and continuing through 2026, allows each team to make one tactical substitution during a match. A player from the pre-named squad of five can replace any member of the playing eleven and bat, bowl or field just like any regular team member. It changed how captains build squads. It also added a new income stream with its own tax treatment.

Under the BCCI Player Regulations 2025-27, every playing member, including the Impact Player, receives a match fee of ₹7.5 lakhs per match, over and above their contracted auction amount. This is separate income, paid per appearance, taxable in its own right. Both the auction contract and the match fee attract 10% TDS under Section 194J and 18% GST under RCM.

Across 14 league matches, the match fee liability alone for a single player is ₹1.05 crore before tax. Across a full squad with regular Impact Player rotations, it becomes a number that belongs in the pre-season financial model, not discovered mid-season.

Every time a captain raises the Impact Player card, the franchise’s compliance calendar gets a new entry. ₹7.5 lakhs, taxed separately, filed accordingly.

The Benched Player: Paid Whether They Play or Not

This is the part that surprises most people outside the industry. A player bought at auction for ₹5 crore who spends the entire season on the bench receives the full ₹5 crore. The auction contract is not performance-contingent. It is a fixed-term professional services contract for the season. The contracted amount is owed regardless of whether the player takes the field.

The match fee is the only component that requires actual playing participation. A benched player earns no match fees. But their auction contract runs, instalment payments are made as per the BCCI-registered schedule, and TDS is deducted on each payment throughout.

For franchise finance teams, this means squad selection carries a direct cost implication. A ₹10 crore signing who plays all fourteen games generates ₹1.05 crore in additional match fee liability. The same player sitting out six games saves ₹45 lakhs in match fees against a ₹10 crore base. Commercially insignificant, but worth tracking in a clean compliance register.

3. Injury Insurance: What Happens When a ₹20 Crore Player Cannot Take the Field

A high-value player going down with an injury mid-season is every franchise’s worst commercial scenario. A ₹20 crore signing who plays three matches and ruptures a hamstring in April is not just a sporting loss. It is a working capital problem the franchise manages while the scoreboard shows zeros against that player’s name.

The IPL runs two distinct layers of insurance for this situation, and they work very differently from each other.

BCCI’s Insurance Scheme: National Duty Injuries

The BCCI maintains an insurance policy covering contracted national team players injured while representing India. If a player is unavailable for the IPL because of an injury sustained during an India series, the BCCI’s insurance compensates the affected franchise for the lost playing availability. The payout flows to the franchise, not to the player as personal income.

Here is a genuinely interesting GST question: if compensation flows because a player is injured and cannot play, is that payment a taxable supply? The answer, after careful legal analysis, is no. The compensation is not a fee for any service. The player never agreed to be injured or to stay off the field in exchange for money. The indemnity is a contractual condition, a promise of financial protection built into the national contract. Since there is no supply of service underlying the payment, GST does not apply to injury compensation payouts.

Franchise Insurance: IPL Season Injuries

For injuries that occur during the IPL season itself, franchises hold their own insurance coverage. If a player goes down mid-season, the franchise may continue paying part of the contract while the insurer covers the remainder, depending on the timing, severity and what the policy covers.

The key point is payment continuity. An injury during the season does not cancel the player’s right to their contracted auction fee. The salary obligation survives the injury. The insurance policy determines how the financial burden is split between franchise and insurer. TDS obligations on the contracted salary continue throughout, regardless of whether the player is fit to play.

4. The ₹18 Crore Ceiling: What the BCCI’s 2026 Mini-Auction Rule Actually Does

The IPL 2026 mini-auction introduced a rule that generated a lot of headlines but was widely misunderstood. Here is exactly how it works.

For overseas players in a mini-auction, the salary they can personally receive is capped at the lower of two figures: the highest retention slab from the previous cycle, currently ₹18 crore, or the highest bid recorded at the previous mega-auction. Since the highest bid at the IPL 2025 mega-auction was the ₹27 crore paid by Lucknow Super Giants for Rishabh Pant, the retention slab is the binding constraint. ₹18 crore is the ceiling. No overseas player takes home more than that, regardless of how high the bidding goes.

The Cameron Green transaction is the clearest illustration. Kolkata Knight Riders bid ₹25.20 crore for Green at the December 2025 auction in Abu Dhabi, making him the most expensive overseas player in IPL history. Green personally receives ₹18 crore. The remaining ₹7.20 crore goes to the BCCI Player Welfare Fund. KKR’s auction purse is reduced by the full ₹25.20 crore.

The franchise pays the full bid. The player does not receive the full bid. The surplus does not return to the franchise. Indian players carry no such cap. Rishabh Pant’s ₹27 crore went to him in full. That asymmetry is deliberate BCCI policy to anchor overseas compensation to the Indian benchmark without restricting how much franchises choose to bid.

5. The Agent’s Fee: The Liability Nobody Budgets For

No marquee overseas signing happens without an agent. The standard range is 5% to 10% of the contract value, and for international players, the agent is typically based offshore. That offshore element creates the compliance exposure that tends to surface during post-season audits rather than pre-season planning.

When a franchise pays a fee to a foreign agent, that payment is classified as an Import of Service under Indian GST law. The franchise is liable to pay 18% GST on the agent’s fee under RCM, in addition to whatever withholding tax applies under the relevant Double Taxation Avoidance Agreement (DTAA) between India and the agent’s country of residence.

On a ₹20 crore player contract with a 10% agent fee, that is ₹2 crore going to the agent and an additional ₹36 lakhs in RCM GST on that fee alone. Across a full overseas roster, the agent liability is a meaningful number that belongs in the pre-auction budget.

6. The Scorecard: The Universal Landing Cost Rule

| Component | Indian Player | Overseas Player |

|---|---|---|

| Winning Auction Bid | ₹20.00 Crore | ₹20.00 Crore |

| BCCI Welfare Fund (Surplus) | Nil | (₹2.00 Crore)* |

| Gross Salary Payable | ₹20.00 Crore | ₹18.00 Crore |

| TDS / Withholding Tax | (₹2.00 Crore) 10% u/s 194J | (₹4.00 Crore) 20% u/s 115BBA |

| Net Pay to Player | ₹18.00 Crore | ₹14.00 Crore |

| GST Outflow (18% RCM) | ₹3.60 Crore | ₹3.60 Crore |

| TOTAL CASH OUTLAY | ₹23.60 Crore | ₹23.60 Crore |

Note: TDS for the overseas player is applied on the full ₹20 crore bid, not just the ₹18 crore the player receives. The ₹2 crore going to BCCI welfare is still part of the taxable payment. Match fees of ₹7.5 lakhs per match and agent fees are additional and calculated separately on top of the above.

7. The 40% GST on Tickets: Why Every Jersey Patch Is Doing Heavy Lifting

This is where GST 2.0 and the IPL collide in a way every fan buying a match ticket felt immediately. Under the GST 2.0 rationalisation effective September 2025, the GST on IPL match tickets increased from 28% to 40%. The government formally classified the IPL as a luxury entertainment event, placing it in the same tax bracket as casinos and race clubs.

A ticket with a base price of ₹1,000 that previously cost ₹1,280 inclusive of 28% GST now costs ₹1,400. A ₹500 ticket costs ₹700. The fan pays more. The franchise collects the tax and remits it to the government. They keep only the base fare.

For every ₹1,400 a fan spends at the gate, the franchise retains ₹1,000 and the government takes ₹400. That is 28.6 paise out of every rupee going straight to the government before the franchise sees it. Ticket revenue was already the smallest slice of a franchise’s income before this change. At 40% GST, it becomes smaller still. Every sponsor logo on the jersey, every brand patch on the kit, every title sponsor activation is compensating for a ticketing structure where the government collects its share first and the franchise works with what remains.

When the government collects ₹400 before the franchise earns ₹1,000, the jersey stops being a uniform and starts being a revenue recovery tool.

8. The Billion-Dollar Balance Sheet: What RCB and RR Are Actually Worth

In March 2026, two franchise sales happened within days of each other that permanently reset what it means to own an IPL team. Royal Challengers Bengaluru was acquired by a consortium comprising Aditya Birla Group, Times of India Group, Bolt Ventures and Blackstone for approximately $1.78 billion (₹16,660 crore), the highest valuation ever paid for a cricket franchise. Rajasthan Royals were acquired simultaneously at a $1.63 billion valuation. Two teams bought for roughly $100 million each in 2008 changed hands in 2026 for a combined $3.41 billion.

What makes these numbers defensible? Three things.

Guaranteed income, regardless of where you finish. Each franchise receives approximately $55 million annually from the BCCI’s central pool under the 2023-27 media rights cycle, a deal worth $6.2 billion in total. That income flows whether the franchise wins the title or finishes last. When core revenue is contractually guaranteed and inflation-linked, the asset is fundamentally easier to value than a conventional business where income tracks market conditions.

No stadium, no infrastructure, no heavy capital cost. IPL franchises do not own their venues. They rent the ground, the floodlights and the outfield. The balance sheet carries operational assets, not capital-intensive infrastructure. In GST terms, the input chain is almost entirely service-based, player contracts, broadcast costs, coaching staff, which keeps ITC reconciliation relatively clean compared to a manufacturing or real estate business.

Genuine, non-replicable scarcity. There are exactly 10 IPL teams. The BCCI does not expand the league casually. There are approximately 1.47 billion people in India with a near-religious relationship with cricket. The 2025 IPL final between RCB and Punjab Kings drew 169 million TV viewers, more than the 2021 India-Pakistan T20 World Cup match. That is not a sporting audience. That is a national-scale media asset with a fixed supply.

In Closing: The Ledger Behind the Spectacle

The IPL is genuinely great sport. The cricket is real, the pressure is real and the moments are real. But so is the tax. Every paddle raised in that auction room triggers a cascade of financial obligations: TDS calculations, RCM cash payments, welfare fund contributions, DTAA checks on agent fees, match fee compliance for every Impact Player appearance, insurance premiums modelled against roster risk. The franchise that manages this cascade cleanly, that builds its landing cost model before auction day and files its obligations on time, is the franchise spending its working capital on cricket rather than on fixing paperwork. In a salary-cap league where every crore matters, compliance discipline is a competitive edge.

Up Next: This post looked at what the franchise spends. Next week, we are looking at how they earn it back sponsorship GST, media rights structuring, and why the taxman is waiting on that side of the ledger too.

Explore all posts at thetaxathlete.com.

Frequently Asked Questions

What is the TDS rate on IPL player contracts for Indian players?

Indian IPL players are treated as Independent Professionals, not salaried employees. The franchise withholds 10% TDS on the full contract value under Section 194J of the Income Tax Act, 1961. This is the player’s advance income tax, deducted before any payment is made.

How is GST applied on payments to IPL players?

Under Section 9(3) of the CGST Act, 2017 read with Notification No. 13/2017-CT(Rate), the franchise pays 18% GST directly to the government under the Reverse Charge Mechanism (RCM) on payments to individual sportspersons. This applies to both Indian and overseas players. The franchise pays the GST in cash first and claims Input Tax Credit in a subsequent return period.

How is an IPL Impact Player paid and is it taxed differently?

An Impact Player receives their regular auction contract amount plus a match fee of ₹7.5 lakhs per match under the BCCI Player Regulations 2025-27. This match fee is separate from the auction contract and taxable in its own right. Both the contract amount and the match fee attract 10% TDS under Section 194J and 18% GST under RCM. A player appearing in all 14 league matches earns ₹1.05 crore in match fees alone, on top of their auction contract.

Does a franchise still pay a player who is benched or injured?

Yes. The auction contract is a fixed-term professional services agreement. A benched or injured player still receives the full contracted auction amount. Only the ₹7.5 lakh match fee requires actual playing participation. For injuries during national duty, the BCCI’s insurance scheme compensates the franchise. For IPL season injuries, franchises carry their own policies. Injury compensation payouts are not subject to GST as they are insurance settlements, not payments for a service rendered.

Why did Cameron Green receive only ₹18 crore when KKR bid ₹25.20 crore?

The BCCI’s 2026 mini-auction rule caps overseas player earnings at the lower of the highest retention slab (₹18 crore) or the highest bid from the previous mega-auction. Since Rishabh Pant’s ₹27 crore in 2025 exceeded ₹18 crore, the retention slab became the binding cap. The remaining ₹7.20 crore was deposited into the BCCI Player Welfare Fund. KKR’s auction purse was still reduced by the full ₹25.20 crore.

What is the GST rate on IPL tickets in 2026?

IPL match tickets attract 40% GST from September 2025 under the GST 2.0 rationalisation. The IPL has been formally classified as a luxury entertainment event, in the same bracket as casinos and race clubs. A ₹1,000 base-price ticket now costs ₹1,400. Tickets priced at ₹500 or below are exempt. International cricket matches played in India remain at 18% GST for tickets above ₹500.