Warm-Up

In an earlier post on the UAE VAT Credit Deadline 2026, we tracked how the Federal Tax Authority introduced a hard five-year window for recovering input tax. Miss that window and the credit is gone permanently. That was a deadline story. This post is different. This is about the complete replacement of how a legal tax invoice is defined in the UAE, starting 1 January 2027 for large businesses. If that earlier post was about the VAT system tightening its recovery rules, this one is about the transactional pipeline itself being rewired from end to end.

For nearly a decade, UAE corporate compliance operated at a comfortable pace. A finance team would compile transaction data across the quarter, prepare a summary VAT return on the EmaraTax portal, and then spend the following weeks correcting discrepancies, chasing documents, and reconciling ledger entries after the fact. The audit regime was retrospective. If something was wrong, there was usually time to fix it.

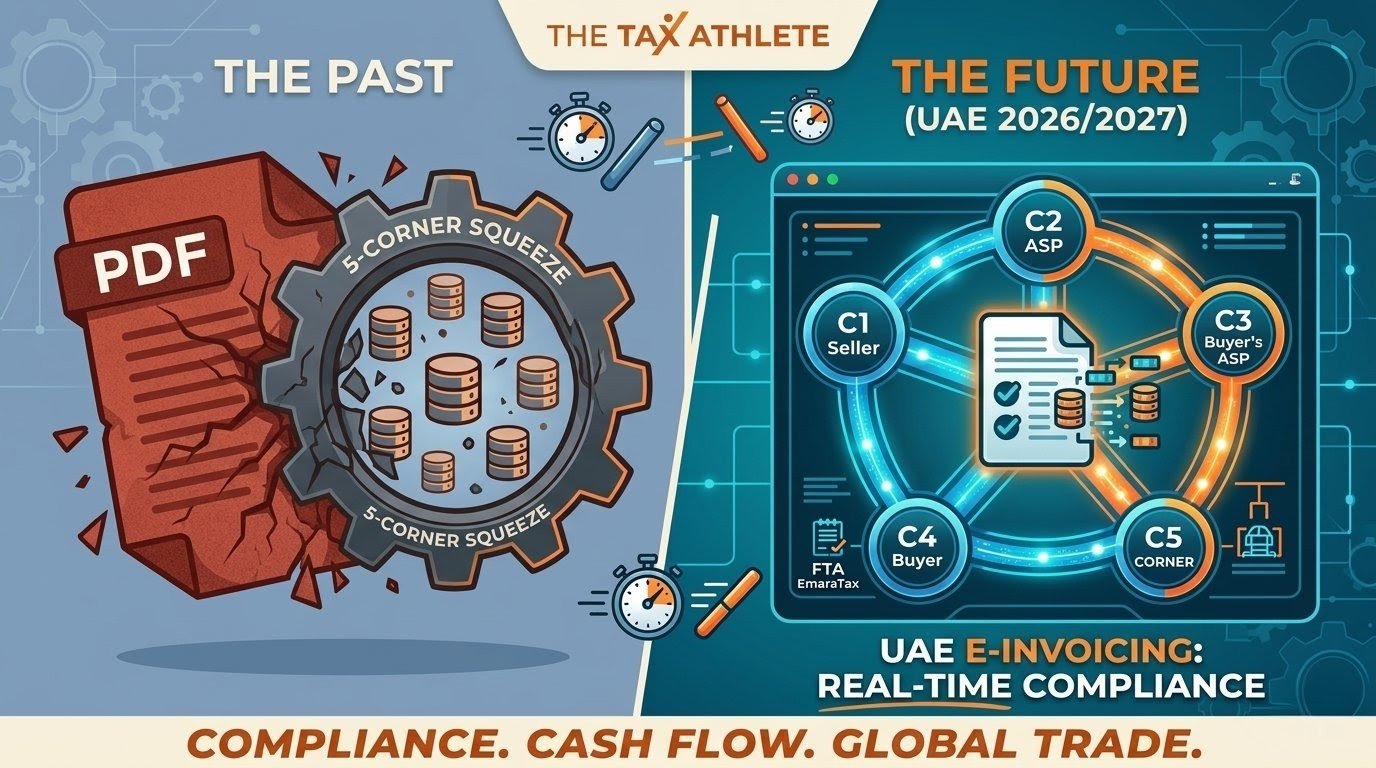

That era officially ends in 2027. The UAE Ministry of Finance and the Federal Tax Authority (FTA) have introduced a Decentralised Continuous Transaction Control and Exchange framework, known as DCTCE. This framework is built on an international invoicing network called Peppol and uses a data standard specifically adapted for the UAE, called PINT-AE. Together, they replace the PDF tax invoice as the country’s legal standard for a business-to-business transaction record.

The shift is not about what an invoice looks like. It is about what an invoice is. Under the new rules, a tax invoice is no longer a document. It is a validated data transmission. And if your business does not have the systems in place to generate that transmission, your invoices do not exist from a legal standpoint, regardless of how professionally formatted your PDF happens to be.

I want to break this down the way I approach any complex regulatory change in my own work: start with the structure, understand the tax consequences at each stage, and build from there. The technology is the delivery mechanism. The tax risk is what actually matters.

1. The 5-Corner Architecture: The FTA Now Watches Every Baton Pass

Most countries that have adopted digital invoicing use what is called a 4-Corner network. Think of it as a relay race. The seller passes the baton to their service provider, the service provider passes it across the network to the buyer’s service provider, and the buyer’s service provider delivers it to the finish line. Four handoffs, four corners.

The UAE has built a fifth corner directly into that relay track. That fifth corner is the FTA itself. In the UAE model, the tax authority does not wait at the finish line to review what happened. It is positioned in the middle of the race, intercepting the transaction data before it ever reaches the buyer.

Corner 5 is not a filing portal you visit once a quarter. It is a permanent, real-time transaction ledger. Any invoice that bypasses this step has no legal existence in the UAE tax system, regardless of what your own accounting records show. If your general ledger shows a sale that the FTA’s ledger does not recognise, you have an audit exposure sitting on your books right now.

In practical terms, this means that the old sequence has been reversed. Previously, a transaction happened, an invoice was issued, and tax was reported afterward. Under the 5-Corner model, the transaction cannot be legally completed until the tax authority has already processed the data. Compliance is built into the beginning of the transaction, not bolted on at the end.

2. Why Your PDF Invoice Is No Longer a Legal Tax Invoice

This is the point that many businesses have not yet absorbed. The question is not whether your PDF invoice looks professional or includes all the right VAT fields. The question is whether it can be processed automatically by the machines at Corner 2 and Corner 5. A PDF cannot. It is an image of information, not structured information itself.

Under the new framework, a valid tax invoice must be a structured, machine-readable data file in XML or JSON format, mapped to the PINT-AE data standard, transmitted through a UAE-accredited service provider. A PDF emailed to a client, no matter how detailed, satisfies none of those conditions. It is the invoicing equivalent of trying to run a digital race with a paper baton.

Under Cabinet Decision No. 106 of 2025, businesses that fail to implement the Electronic Invoicing System face an administrative penalty of AED 5,000 per month (or part thereof) until the system is operational. There is also a separate penalty of AED 100 per individual invoice that is issued but not transmitted through the system, capped at AED 5,000 per calendar month. These penalties run concurrently if multiple violations occur simultaneously.

The implication for tax directors is straightforward but uncomfortable. If your billing platform today outputs a PDF and sends it by email, you are not partially compliant. You are fully outside the legal invoicing framework that will apply from 1 January 2027 for businesses with annual revenue of AED 50 million (approximately USD 13.6 million) or more. Businesses below that threshold enter the mandatory phase from 1 July 2027.

3. The PINT-AE Data Dictionary: A Tax Audit Hidden Inside a Data File

The part of this transition that tends to get lost in conversations about technology is that the PINT-AE data standard is not primarily an IT specification. It is a detailed description of exactly what tax information the FTA expects to receive for every transaction, in exactly what format, at the moment the transaction occurs.

The data dictionary defines more than 135 data elements, of which approximately 50 are mandatory for a standard tax invoice. Several of those mandatory fields are entirely new from a compliance standpoint. They require businesses to make active tax decisions at the point of billing that were previously made retrospectively, if at all.

Four areas deserve particular attention because they represent genuine tax risk, not just technical inconvenience.

Free Zone Transactions

The PINT-AE schema requires your billing system to flag whether a transaction originates from or terminates in a Designated Free Zone, and to apply the correct VAT treatment automatically. If the geographic coding is absent or wrong, the system defaults to the standard 5% rate. That creates a reconciliation error and a potential audit assessment if the correct treatment was actually zero-rated or out of scope.

Deemed Supplies

Business assets put to private use, free samples distributed to clients, and corporate gifts above the prescribed threshold are all deemed supplies under UAE VAT law. These events must now generate validated e-invoices tagged with the correct deemed supply identifier. The VAT liability is calculated on cost price, not a commercial sales price. Without this flag, these transactions route through as standard revenue lines, distorting your gross margin data and creating exposure during corporate tax assessments.

Continuous Supplies

Long-term service contracts, phased construction projects, and recurring monthly retainers are classified as continuous supplies. The PINT-AE schema requires mandatory start and end dates for the service period in these cases. The FTA uses those dates to verify that the tax point matches the underlying contract milestones. If the dates are missing, the system treats the invoice as a single-point transaction. The resulting timing mismatch can trigger penalties during an external audit.

Foreign Currency Conversion

If you bill an international client in USD, EUR, or GBP, showing the foreign currency amount is not sufficient. The PINT-AE data dictionary requires the exact AED equivalent of every line item, calculated using the official daily exchange rate published by the UAE Central Bank, to be injected into the transaction data at the line level. A rounded conversion or an approximation will cause a validation rejection at Corner 2.

The practical consequence is that tax professionals must define the business rules that drive these decisions before the billing system ever generates an invoice. This is not something that can be delegated entirely to an IT implementation team. The classification of whether a transaction is a deemed supply, the determination of which free zone rules apply, and the logic for identifying a continuous supply are all tax judgements. If those judgements are encoded incorrectly into the system’s logic, every invoice produced by that system becomes a self-generated audit finding delivered directly to the FTA in real time.

4. The Dual-Billing Transitional Trap: When Your Client Has Not Yet Caught Up

A reasonable assumption from many Phase 1 businesses is that once their own systems are upgraded, the work is complete. This overlooks the reality that a significant portion of the UAE’s business population, particularly mid-market firms, boutique agencies, and smaller enterprises, will not be connected to the Peppol network when the mandatory phase starts.

The 2026 guidelines address this directly. If a buyer is not yet registered on the Peppol network, the supplier cannot route the transaction through the standard 5-Corner flow. Instead, the supplier must simultaneously execute two separate workflows:

First, the supplier’s system must transmit the structured XML data directly to the FTA through a designated fallback endpoint, ensuring the tax liability is registered at Corner 5 even without a buyer-side ASP in the loop. Second, the supplier must generate a human-readable, compliant commercial PDF and deliver it directly to the buyer through traditional channels so the buyer can process payment.

If a supplier transmits the XML to the FTA but fails to deliver the PDF to the buyer, the buyer has no payment-triggering document. If a supplier delivers the PDF to the buyer but fails to transmit the fallback data to the FTA, that PDF is technically invalid as a tax invoice. A buyer who realises the transaction is unregistered at Corner 5 can legally refuse payment to protect their own input tax recovery position. Incomplete dual-billing execution is a direct cash flow risk, not merely a compliance risk.

Managing this transition manually, by sorting clients into a Peppol list and a PDF list and handling them separately, is operationally unsustainable at any meaningful transaction volume. The correct approach is an automated counterparty verification check built into the accounts receivable workflow. Before any billing run is finalised, the system queries a current register of onboarded buyers and routes the transaction accordingly. Businesses that do not build this check in advance will face significant manual workload during exactly the period when implementation pressure is already highest.

5. The 24-Month Intercompany Grace Period: A Rest Day, Not a Holiday

Corporate groups reviewing the February 2026 guidelines will have noticed a 24-month grace period for intra-VAT group transactions, running from 1 January 2027 to 31 December 2028. This means that e-invoicing obligations for transactions between members of the same VAT group are temporarily suspended during that window.

Some finance teams have interpreted this as a two-year exemption from the e-invoicing framework for all intercompany activity. That interpretation is incorrect and could prove expensive.

The grace period applies specifically to intra-VAT group transactions. It does not apply to transactions with external counterparties or other business activities. More importantly, those intercompany transactions remain fully within the legal scope of the e-invoicing regime. The grace period suspends active enforcement penalties during the transition window. It does not suspend the underlying legal obligation.

In training terms, this is the equivalent of a scheduled deload week. Active work volume drops, but the training framework is still in place. A deload week is not permission to abandon your technique. When full intensity resumes, your mechanics need to be ready.

The operational danger is this. If a business upgrades its external billing engine to handle PINT-AE structured data while leaving its intercompany recharge workflows on legacy batch formats, it creates a split architecture. When the grace period ends on 31 December 2028, the finance team will face the task of retroactively mapping years of unmapped intercompany transactions into compliant data structures. During any formal tax audit, the FTA reviews the full entity ledger, not just external sales. Running two different data standards simultaneously creates clear inconsistencies and opens exposure across the entire audit period.

Transactions between members of the same UAE VAT group. The suspension of enforcement penalties applies only within that defined perimeter. Intercompany recharges to entities outside the VAT group, management fees to third parties, and all external B2B transactions are fully in scope from day one.

6. Why Tax Directors Must Own This, Not Just the IT Team

The framing of e-invoicing as an IT project is the single most dangerous misconception about this transition. The technology is the plumbing. What flows through that plumbing is a series of tax decisions that, under the 5-Corner model, are made automatically and irreversibly at the moment each transaction occurs.

Consider how message-level rejections work in practice. When an invoice is rejected by the Corner 2 ASP, whether for a missing tax code, a wrong free zone flag, or a miscalculated line extension amount, the system responds within minutes. The rejection is immediate and automated. The commercial transaction has already occurred. The goods have shipped, the service has been delivered, but the invoice does not legally exist.

Resolving that situation requires issuing a corrected invoice with a fresh sequential number, potentially raising a credit note against the rejected transaction, and ensuring the correction does not create a timing mismatch against any contractual payment terms. The governance for how the finance team handles that sequence, without breaking compliance or disrupting cash flow, is entirely a tax director’s responsibility. No software platform will make those calls automatically and correctly without a documented tax decision framework behind it.

Tax teams must also sign off on the tax matrix that drives the system’s automated decisions: which product lines qualify for standard rate, which are zero-rated, which are exempt, and which fall outside scope entirely. If an IT mapping exercise translates those classifications incorrectly for the sake of making the technical validation pass, the business has created a perfectly formatted, legally delivered, self-incriminating audit record.

7. Your Pre-Season Training Plan: What to Prioritise Before January 2027

Businesses with annual revenue of AED 50 million or more must appoint a UAE Accredited Service Provider and register on EmaraTax. Missing this date triggers the AED 5,000 monthly penalty immediately, even before the January 2027 go-live. The pilot phase has been open since 1 July 2026 for voluntary early adoption.

Map your current ERP fields against the approximately 50 mandatory PINT-AE schema fields. Identify every field where your existing data is incomplete, inconsistent, or formatted incorrectly. Pay particular attention to buyer tax registration numbers, free zone indicators, supply type classifications, and the currency conversion logic for foreign-denominated billing.

Document the tax treatment of every product line and service category in your billing system. Identify all deemed supply events in your operations. Review all continuous supply contracts and confirm that start and end date fields are captured in your customer master data. This is the tax matrix that will drive every automated decision once the system goes live.

Begin categorising your client base by Peppol onboarding status. Design the dual-billing workflow for clients who will not be connected by January 2027. Build the automated routing logic into your accounts receivable process before the mandatory date, not in response to the first rejected invoice.

Do not defer intercompany integration because of the grace period. Begin mapping internal recharges, management fees, and shared service cost allocations to the same PINT-AE validation schemas used for external transactions. Build a clean, unified internal data standard now so that the grace period end date does not create a retroactive data remediation crisis.

Mandatory go-live for Phase 1 businesses with revenue of AED 50 million or more. Only structured XML invoices transmitted through a Peppol-connected ASP and validated at Corner 5 constitute legal tax invoices from this date. PDF-only billing workflows become non-compliant.

Mandatory compliance extends to all other in-scope businesses, including smaller VAT-registered entities. Free zone businesses are included in this mandate unless they conduct exclusively B2C transactions.

8. Before and After: The Operational Shift in Plain Language

| Dimension | Legacy Approach (Pre-2027) | DCTCE Approach (From 2027) |

|---|---|---|

| What Counts as a Legal Invoice | Human-readable PDF or printed tax invoice | Validated XML/JSON data file transmitted through an ASP and registered at Corner 5 |

| When the FTA Knows About It | When you file your quarterly VAT return | At the moment of the transaction, in near real time |

| Currency Handling | Foreign currency total on invoice face, optional conversion note | Line-by-line AED conversion using the official UAE Central Bank daily rate, embedded in the data |

| Fixing an Error | Retrospective credit note or amended return, often weeks later | Instant rejection at Corner 2 if validation fails; new invoice with fresh sequential number required before transaction is legally registered |

| Non-Compliance Penalty | Standard VAT penalty regime applied retrospectively | AED 5,000 per month for system non-implementation; AED 100 per invoice not transmitted (capped at AED 5,000 per month) |

| Intercompany Billing | Internal journal entries or manual batch invoicing | Required to meet PINT-AE standards; 24-month grace period for intra-VAT group transactions only |

The Tax Athlete Takeaway

In competition, the athletes who underperform are rarely those who lacked talent. They are the ones who treated the preparation phase as optional. The 5-Corner e-invoicing model is the UAE’s most significant VAT infrastructure change since 2018. The businesses that treat it as a January 2027 IT project will arrive at the start line without having done the conditioning work.

The conditioning work here is the tax classification exercise, the data field mapping, the counterparty readiness check, and the intercompany architecture review. None of those steps belong to IT. All of them belong to the tax director.

A PDF invoice beautifully formatted and correctly totalled is now legally insufficient. What replaces it is not more complex from a tax logic standpoint. But it requires that tax logic to be captured in structured, machine-readable data before the invoice leaves the building. That is the transition. And the time to build for it is now, not in December 2026.

References

Abdellatif, M. (2024). Assessing value added tax compliance burden in Gulf Cooperation Council countries. eJournal of Tax Research, 22(1), 295–315.

Ainsworth, R. T., & Alwohaibi, M. (2016). GCC VAT: The Intra-Gulf Trade Problem. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2916252

UAE Ministry of Finance. (2026, February 23). Electronic Invoicing Guidelines. Ministry of Finance, UAE.

UAE Ministry of Finance. (2025). Cabinet Decision No. 106 of 2025 on Administrative Penalties for the Electronic Invoicing System.

UAE Ministry of Finance. (2025). Ministerial Decision No. 243 of 2025 and Ministerial Decision No. 244 of 2025 on the Electronic Invoicing System.

Alvarez & Marsal. (2026, February 25). UAE Electronic Invoicing Guidelines: February 2026 Regulatory Clarifications and Technical Implementation Framework. Retrieved from alvarezandmarsal.com