The Warm-Up: Where We Left Off

Last week, we tracked how Indian businesses can protect their margins when crude hits $100 and the rupee weakens. Before that, we broke down why domestic manufacturers can finally stop chasing their own GST refunds under the Finance Bill 2026. Both of those posts dealt with pressure from outside the system. Today, we are looking at the biggest structural change inside the system itself. The GST framework that India has operated on since 2017 has just been fundamentally redesigned and if your business has not already started updating its rate masters, this post is urgent reading.

The 60-Second Version

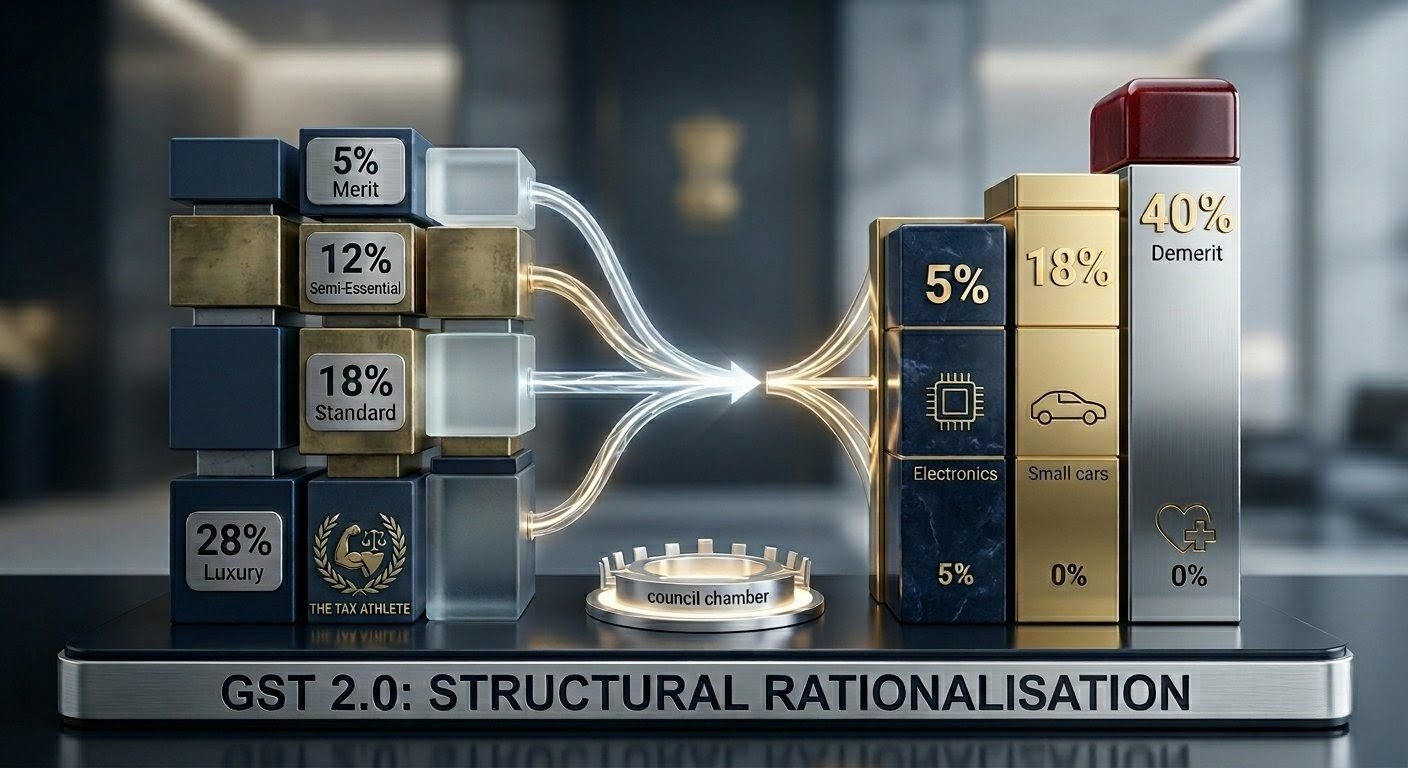

- India has moved from 4 GST slabs (5%, 12%, 18%, 28%) to 3 slabs: 5%, 18%, and 40%

- The 12% slab is gone. Most items have moved down to 5% including surgical equipment, FMCG, and farm machinery

- The 28% slab is gone. Most items have moved down to 18% including ACs, TVs, and small cars

- A flat 40% rate replaces the old “28% plus Compensation Cess” for luxury and sin goods

- Life and health insurance premiums are now at 0% GST

- New post-sale discount rules give businesses more flexibility on credit notes

If you have ever sat across a table from a tax officer and argued about whether your product is a “12% essential” or an “18% standard supply,” you already understand why GST 2.0 is a relief. I have been in those rooms. That six-percentage-point grey zone has fuelled years of disputes, litigation and reassessments that nobody needed. The 2026 rationalization closes it for good.

This is not a rate adjustment. It is a structural rethink of how India taxes goods and services, and it has real consequences for your pricing, your Input Tax Credit and your compliance workload. Let us go through it properly.

At a Glance: Old Slabs vs. New Slabs

| Old Slab | New Slab | What Moved |

|---|---|---|

| 5% Merit | 5% Merit | Retained and expanded to absorb most 12% essentials |

| 12% Semi-essential | Abolished | Surgical equipment, dairy, farm machinery moved to 5% |

| 18% Standard | 18% Standard | Retained. Now covers ACs, TVs, and small cars too |

| 28% Luxury + Cess | 40% Demerit | Luxury SUVs, tobacco, aerated drinks. Cess merged in |

1. Why Were the 12% and 28% Slabs Removed?

To understand this, you need to think about what “Rate Overlap” actually meant in practice and I mean in the trenches, not in a circular.

For nearly a decade, the 12% and 18% slabs sat right next to each other. Close enough that businesses and their lawyers constantly argued about which side of the line a product fell on. Was your product an “essential service” deserving the 12% rate or a “standard supply” at 18%? A six-percentage-point difference on crores of turnover is worth fighting over and fight they did. I have seen clients spend more on legal fees contesting a classification than the tax saving was even worth.

The government was also dealing with the Inverted Duty Structure (IDS), a problem I have written about in detail. By merging the 12% and 18% rates into a unified 18% chain for most industrial goods, the clog in the credit system is cleared at its root rather than managed through refund queues.

And the revenue maths had to work. The government offset the revenue lost by dropping rates on essentials by pushing luxury goods to a flat 40% rate, keeping overall collection neutral.

2. The 5% Slab: What Moved Down and Why

Almost everything that was sitting at 12% has now come down to 5%. The government calls this the “Merit Rate,” intended for goods that serve the common person and the wider economy.

Surgical Equipment and Diagnostics

Diagnostic kits, medical-grade oxygen and surgical instruments were previously taxed at 12%. They are now at 5%. This directly lowers procurement costs for hospitals and clinics, making healthcare delivery more affordable across the supply chain.

FMCG and Agricultural Goods

Ghee, cheese, processed milk products and organic manure, all previously at 12%, are now at 5%. Tractors and most agricultural machinery have made the same journey down.

The direct effect is lower input costs for farmers and a slightly lighter grocery bill for the urban middle class. The government is explicitly using the tax rate as an inflation-fighting tool and this is the most visible expression of that intent.

3. The 18% Slab: India Redefines What a Luxury Actually Is

The 18% rate is now where roughly 90% of the old 28% category lives. The government has made a clear policy statement with this move: what was once considered a luxury is now acknowledged as a standard household need.

Consumer Electronics

Air conditioners, refrigerators and large-screen televisions above 32 inches have moved from 28% to 18%. That is a 10-percentage-point cut on products that millions of Indian households either own or are actively saving to buy.

An air conditioner in a Delhi summer is not a luxury. The government has finally acknowledged what most households already knew.

For businesses in this space, the price reduction is a genuine commercial moment. The rate cut will not automatically reach your customers unless you reprice. Early movers capture the goodwill and the volume surge. Late movers just look like they are protecting margin.

The Automotive Relief

Small petrol cars under 1200cc and diesel cars under 1500cc have moved from 28% to 18%. A 10% rate drop on an entry-level car is not cosmetic. It translates to a meaningful price reduction for first-time buyers, which drives volume for manufacturers and makes the category accessible to a significantly larger pool of customers.

4. The 40% Slab: One Number Replaces a Formula

The old 28% category had an annoying quirk. The actual tax burden was rarely 28%. On top of the base rate, a Compensation Cess applied to luxury goods, making the real rate anywhere from 35% to 53% depending on the item. Calculating this correctly was messy. Auditing it was messier and the risk of getting the Cess calculation wrong sat on every high-value invoice.

GST 2.0 fixes this with a flat 40% rate. No Cess. No separate calculation. One number.

This applies to luxury SUVs, premium motorcycles above 350cc, cigarettes and tobacco products, and aerated beverages.

5. The Post-Sale Discount Change: The Procedural Engine Behind the Structural Shift

A structural overhaul only works if the day-to-day procedures can keep up with it. One of the quieter but more commercially significant changes in Budget 2026 is how post-sale discounts are now handled under Sections 15 and 34 of the GST Act.

Previously, claiming GST benefits on a discount offered to a customer after the sale required a pre-signed agreement for every individual transaction. This made dynamic commercial deals, festive season schemes and year-end target discounts legally complicated to execute cleanly from a GST perspective. The paperwork requirement was so rigid that many businesses simply avoided structuring discounts in a way that would let them recover the GST on them.

The new rule removes that rigidity. You can now issue credit notes and claim the corresponding GST benefit without a pre-signed agreement for each transaction, as long as the recipient reverses the Input Tax Credit they claimed. I have covered this in detail in an earlier post: Budget 2026: Why the New GST Post-Sale Discount Rules are a Game Changer.

6. Your Compliance Checklist for 2026

Knowing the change is half the job. Here is what needs to happen in your business right now and what the cost of not acting looks like for each one.

GST 2.0 Action Checklist

- HSN Master Overhaul: Update your ERP or accounting software to remove the 12% and 28% categories. These are now defunct for most products. Note that certain construction materials including AAC blocks and building bricks have been retained at 12% as a special rate. If your business operates in the construction materials space, verify your specific HSN classification before updating your rate masters. If you get this wrong, every invoice you raise carries the wrong rate. That is not just a compliance risk; it is a customer dispute waiting to happen.

- Price List Revisions: For any product that moved from 28% to 18%, review and update your pricing. The rate cut is a commercial opportunity and a competitive signal. If your competitors reprice before you do, they capture the demand surge. You lose volume you should have won.

- Monitor ITC Accumulation: If your product moved from 18% input costs to a 5% output rate, you are now in an Inverted Duty scenario. Use the new Rapid Refund facility to recover stuck credits before they compound. Leaving this unmanaged ties up working capital that your business should be deploying, not parking inside a government queue.

- Insurance on Your Payroll: Life insurance and health insurance premiums paid by employers are now at 0% GST. Update your payroll and finance systems immediately. Continuing to charge GST on these benefits means you are overcollecting from employees and creating a compliance exposure for the company.

- Credit Note Process Review: With the new post-sale discount rules, update your commercial agreements and internal finance processes to take full advantage of the flexibility on credit notes. Not updating this means you are leaving GST recovery on the table every time you offer a post-sale incentive to a customer.

In Closing: A Mature Framework. Your Moment to Move First.

India’s GST regime spent its first eight years in test-and-adjust mode. Two slabs, four slabs, changing cess rates, classification disputes that ran for years. What GST 2.0 represents is the system finally settling into a stable posture. Three slabs, cleaner boundaries and procedural rules that match how businesses actually operate.

Every GST amendment has a window. The professionals who came out ahead were not the ones who understood it best in December. They were the ones who updated their systems, repriced their products and filed clean returns in the first month. Speed of execution after a structural change is itself a competitive advantage.

Up Next: The IPL auction table looks like sport. But underneath it, it is one of the most complex indirect tax ecosystems in India. Next week, I am breaking down the economics of IPL, how GST structures influence franchise budgets, player contracts and the hidden tax cost behind every big-ticket signing. If you thought tax was boring, wait until we put it in a jersey.

Explore all posts at thetaxathlete.com.

Frequently Asked Questions

What is the new GST rate on air conditioners in 2026?

Air conditioners have moved from 28% to 18% under GST 2.0, effective from the Union Budget 2026. This applies to all standard residential and commercial units.

Has the 28% GST slab been completely removed?

Yes. The 28% slab has been abolished. Most items in that category have moved to 18%. Luxury and sin goods such as tobacco, aerated beverages, and premium SUVs now attract a flat 40% rate, which also absorbs the old Compensation Cess that used to be calculated separately.

What is the GST rate on small cars in 2026?

Small petrol cars under 1200cc and diesel cars under 1500cc have moved from 28% to 18% under GST 2.0. This is a significant relief for first-time buyers and a volume driver for entry-level automobile manufacturers.

Is GST still applicable on life insurance premiums?

No. Life insurance and health insurance premiums are now at 0% GST under GST 2.0. Employers who have been deducting GST on these benefits through payroll must update their systems immediately to stop this deduction.

What happened to the 12% GST slab?

The 12% slab has been abolished entirely. Items that were in this category, including diagnostic kits, surgical instruments, dairy products such as ghee and cheese, organic manure, and agricultural machinery like tractors, have all moved to the 5% slab. Note that certain construction materials including AAC blocks and building bricks have been retained at 12% as a special rate. If your business operates in the construction materials space, verify your specific HSN classification before updating your rate masters.

What is an Inverted Duty Structure and does GST 2.0 fix it?

An Inverted Duty Structure occurs when the GST rate on your inputs is higher than the rate on your outputs, causing Input Tax Credit to accumulate faster than it can be used. GST 2.0 addresses this for many industrial categories by moving both inputs and outputs to the same 18% rate. For categories where an inversion still exists, the new Rapid Refund facility helps recover stuck credits faster. I have covered this in detail in my GST Refund post.