In EMEA E-Invoicing: Preparing for the ViDA Shift, we tracked how the EU is rebuilding its VAT backbone around digital invoices. Before that, in The Green Ledger: Understanding CBAM for Indian Manufacturers, we showed how carbon costs are now baked into the price of your EU exports. Both posts are about data the EU collects from you directly. This post is about something different: DAC7 & DAC8 data the EU collects about you, from the platforms you use, without you doing anything at all.

triggers reporting

before EU reports you

collection year

Think of it like a cricket match where the third umpire starts reviewing every ball you bowl, not because anyone appealed, but because the system now reviews automatically. That is the world DAC7 and DAC8 have created for Indian businesses selling to European customers.

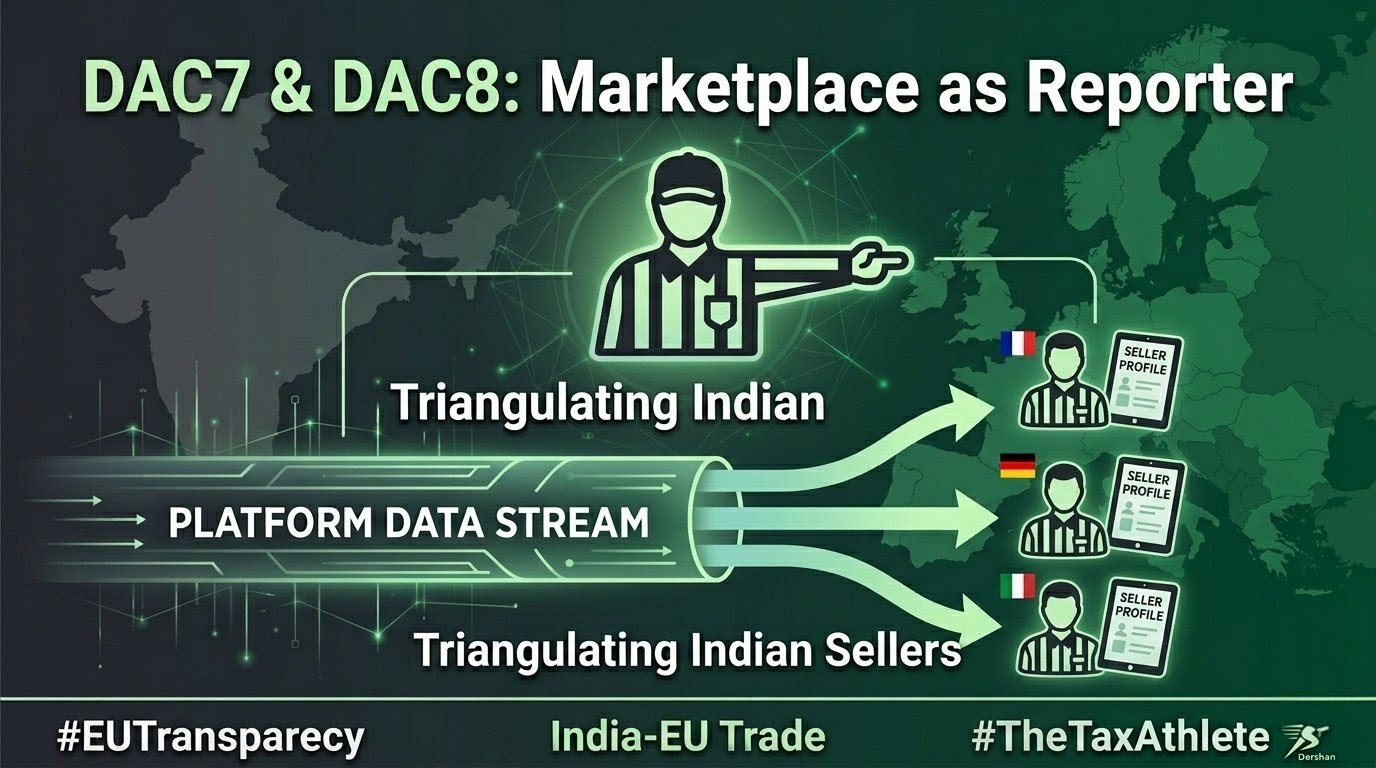

The European Union has spent years building a web of tax transparency tools. We have already covered how ViDA digitises invoices and how CESOP tracks payment data. Now a third data stream has gone live: one generated entirely by the platforms you use, sent directly to EU tax authorities, whether you know about it or not. If you sell on Amazon, provide services on Upwork, or use crypto to settle international invoices, this post is your field guide.

Understanding the DAC Framework

The Directive on Administrative Cooperation, or DAC, is the EU’s primary legal engine for tax transparency. Think of it as the rulebook that tells EU member states how to share tax data with each other and with trading partner countries. Early versions of the DAC focused on traditional bank accounts and employment income. The newer versions target the digital economy, where income is far harder to trace.

DAC7 is Council Directive (EU) 2021/514. It came into force on 1 January 2023. It requires digital platform operators to collect information on sellers and report that information to EU tax authorities every year. The first round of reports was submitted in January 2024, covering all seller activity from 2023 onward. The scope of DAC7 is wide: it applies to platforms based inside the EU and outside the EU, as long as they facilitate transactions involving EU sellers or EU-located property.

DAC8 extends the same logic to crypto assets. Adopted on 17 October 2023, it requires Reporting Crypto-Asset Service Providers (RCASPs) to collect data on users’ transactions starting 1 January 2026. The framework is built on the OECDOrganisation for Economic Co-operation and Development. An intergovernmental body of 38 countries that sets global standards for economics and taxation. Its Crypto-Asset Reporting Framework (CARF) forms the technical foundation of DAC8.‘s Crypto-Asset Reporting Framework (CARF). The first actual exchange of information between EU tax authorities and other countries is scheduled by 30 September 2027. DAC8 closes the final major gap in the EU’s digital tax net.

“DAC7 does not create any new tax. It is a tool that lets tax authorities cross-check what a seller declares against what the platform says they earned.”

The Four Activities That Trigger DAC7 Reporting

Not every website qualifies as a “platform” under DAC7. Reporting only kicks in when a platform facilitates one of four specific activities in exchange for a fee:

The most common category for Indian exporters. Selling handcrafted textiles, electronics, or any physical product through Amazon, eBay, or Etsy to EU households falls here.

Software development, tutoring, consulting, or any professional work performed via platforms like Upwork or Fiverr. Even work billed in USD counts if the service is delivered to an EU client.

Primarily relevant for Airbnb or Booking.com hosts. Indian entities owning EU holiday rentals or commercial spaces are caught here regardless of where they are tax-resident.

Car sharing, equipment rental, and similar peer-to-peer platforms operating across EU borders. Less common for Indian businesses but growing with Web3 logistics models.

Who Exactly Is a “Reportable Seller”?

For an Indian business, the question that matters most is whether the platform must report your specific data. Under DAC7, you become a reportable seller once you cross 30 transactions or EUR 2,000 in total sales in a calendar year on that platform. Below both of those numbers, you are excluded as a casual seller. The moment you cross either limit, the platform is legally required to collect your legal name, address, Indian PAN or GSTIN, bank account details, and total consideration received and send that to an EU tax authority.

For non-EU residents like Indian sellers, the clearest trigger is selling goods to EU consumers through a platform, or renting out property located within the EU. You do not need to be physically present in Europe for the reporting obligation to bite.

The Equivalence Mechanism: What It Means for Indian Platforms

One lesser-known provision of DAC7 is the equivalence mechanism. A non-EU platform operator can be exempt from EU reporting if two conditions are met: first, the platform already reports equivalent data to its home country’s tax authority; and second, that home country has a “Qualified Substantial Agreement” with the EU. The EU Commission assesses and formally declares equivalence through a regulatory process set out in Commission Implementing Regulation (EU) 2023/823.

As of 2026, India does not hold a formal DAC7 equivalence determination from the EU. This means Indian-origin platforms that serve EU customers cannot claim exemption from DAC7 registration. They must register in a single EU member state and report seller data from there. This “long arm” jurisdiction is something many Indian tech companies and marketplaces have not yet accounted for in their compliance frameworks.

Two Case Studies: The Indian Reality on the Ground

Case Study A: The Amazon FBA Seller from Jaipur

A business in Jaipur sells handcrafted textiles through Amazon Germany using the Fulfilment by Amazon (FBA) model. The goods are shipped from Jaipur to a German warehouse, then delivered locally to German buyers.

Under DAC7, Amazon must report this seller’s data to the German Federal Central Tax Office. That report includes the seller’s Indian GSTIN, PAN, and total gross consideration received for the year.

Storing inventory in a German warehouse before sale creates a VAT registration obligation in Germany. The German local delivery is not an export from India. If the Jaipur seller has been treating these sales as export of goods from India (zero-rated under GST) while the goods physically move within Germany, the DAC7 report creates an automatic mismatch. German authorities can issue a VAT assessment and penalties without even requesting a special audit. The data lands in their system and the discrepancy is visible immediately.

Case Study B: The Tech Consultant on Upwork

A freelance developer in Bengaluru provides AI consulting to a French client through Upwork. The invoice is in USD. The payment arrives in a savings account in India.

Upwork is a personal services platform under DAC7. Every euro-equivalent earned through the platform is a data point. Upwork reports the gross consideration to the relevant EU member state authority. That authority then shares the income data with India’s CBDTCentral Board of Direct Taxes. India’s apex statutory authority under the Ministry of Finance that administers income tax and corporate tax through the Income Tax Department. It receives foreign income data from other countries through international exchange agreements. through the existing automatic exchange of information framework.

If the developer has not reported this foreign income in their Income Tax Return, or has not treated it as export of services under Indian GST, the incoming data from the EU creates a clear gap in their record. The currency in which you were paid does not matter. What matters is whether the income shows up correctly in Indian filings. If it does not, the CBDT now has the EU’s version of the truth.

DAC8 and the Crypto Data Net

Many Indian tech businesses and Web3 startups have used stablecoins or crypto assets to manage international liquidity, pay remote contractors in other countries, or receive payments from global clients. DAC8 treats all of this as a reportable transaction.

Under DAC8, any Reporting Crypto-Asset Service Provider (RCASP) with EU-resident clients must collect the legal name, address, and Tax Identification Number of those users and report all their transactions. Critically, this obligation extends to global exchanges like KrakenA US-based cryptocurrency exchange founded in 2011 and one of the largest globally. If you hold a corporate wallet on Kraken and transact with EU clients, Kraken must report those transactions to the relevant EU tax authority under DAC8. or BinanceThe world’s largest cryptocurrency exchange by trading volume, incorporated in the Cayman Islands. Under DAC8, any exchange serving EU-resident users must report those users’ transaction data to EU tax authorities, regardless of where the exchange is incorporated. if they have EU users, regardless of where those exchanges are incorporated.

What this means for an Indian business: if you receive payment in USDTTether (USDT) is a stablecoin pegged 1:1 to the US Dollar. It is widely used for international crypto settlements because its value does not fluctuate like Bitcoin or Ethereum. Under DAC8, receiving USDT from an EU client through a regulated exchange is a reportable transaction. or any other stablecoin from a French or German client through a global exchange, that exchange will report the transaction to the relevant EU tax authority, which will share it with India. The reporting obligation covers all exchange transactions, transfers, and certain holdings. The first data collection year is 2026, with the first exchange of information between countries due by 30 September 2027.

DAC8 puts a corporate crypto wallet on the same reporting footing as a traditional bank account. The anonymity that the decentralised nature of crypto once provided no longer exists for EU-connected transactions.

- OECD

- Organisation for Economic Co-operation and Development. An intergovernmental body of 38 member countries headquartered in Paris, France, founded in 1961. It sets global policy standards in economics, trade, education, and taxation. In the context of this post, the OECD published the Crypto-Asset Reporting Framework (CARF) in 2023, which forms the technical and legal foundation on which DAC8 is built. India is not a full OECD member but participates actively as an associate economy and follows several OECD tax frameworks including the Common Reporting Standard (CRS) for automatic exchange of financial information.

- CBDT

- Central Board of Direct Taxes. India’s apex statutory authority constituted under the Central Board of Revenue Act, 1963. It functions under the Department of Revenue, Ministry of Finance, and is responsible for administering income tax and corporate tax laws through the Income Tax Department. For the purposes of this post, the CBDT is the Indian authority that receives foreign income and asset data shared by other countries through automatic exchange of information agreements. When an EU member state shares DAC7 or DAC8 data with India, it is the CBDT that processes and acts on that information.

- USDT (Tether)

- Tether (USDT) is a stablecoin, meaning it is a type of cryptocurrency whose value is pegged 1:1 to the US Dollar. It is issued by Tether Operations Limited and is one of the most widely traded digital currencies in the world. It is commonly used for cross-border settlements because it does not fluctuate in value the way Bitcoin or Ethereum does. Under DAC8, receiving USDT from an EU-resident client through any regulated crypto exchange is a reportable transaction, even if you think of it simply as a dollar-equivalent payment.

- Kraken

- A US-based cryptocurrency exchange founded in 2011, headquartered in San Francisco, and one of the oldest and most regulated crypto exchanges globally. It operates in multiple jurisdictions including the EU. Under DAC8, Kraken must collect and report the transaction data of its EU-resident users to the relevant EU tax authorities. If an Indian business receives crypto payments from an EU client through Kraken, that transaction enters the DAC8 reporting chain.

- Binance

- The world’s largest cryptocurrency exchange by trading volume, originally founded in 2017 and incorporated in the Cayman Islands. It serves hundreds of millions of users worldwide, including a substantial EU user base. Under DAC8, Binance is required to report EU-resident users’ transaction data to the relevant EU member state tax authority regardless of where Binance itself is incorporated. This extraterritorial reach of DAC8 is one of its most significant features for Indian businesses that use global platforms for cross-border crypto settlements.

The Triangulation Strategy: Three Data Streams, One Picture

To understand why this matters so much, you need to see how EU tax authorities actually use this data. They do not rely on any single report. They cross-reference three independent data streams simultaneously. This is what compliance professionals call triangulation.

| Data Stream | Source | What It Tells Authorities |

|---|---|---|

| ViDA | Your own digital invoice | What you say you sold. Under ViDA’s Digital Reporting Requirements, mandatory real-time reporting for cross-border B2B transactions becomes effective from July 2030. |

| CESOP | Your bank or payment processor | What the bank says you received. CESOP monitors all cross-border payments into and out of the EU above the reporting threshold. |

| DAC7 | The marketplace or platform | What the platform says you earned. Gross consideration reported annually, independent of your own filings or bank records. |

If your ViDA invoice says EUR 1,000 but the platform reports EUR 1,500 and the bank confirms EUR 1,500, the EUR 500 gap is an automatic red flag. For an Indian exporter, this level of cross-referencing is entirely new. The system does not need a tax officer to spot the discrepancy. It happens algorithmically, and the risk score attached to your business rises the moment the mismatch appears.

Operational Friction Points for Indian Businesses

The Deemed Supplier Problem: In many EU transactions, the platform itself is the “deemed supplier” for VAT purposes. Amazon or Etsy collects and remits VAT to the EU government on your behalf. However, the platform still reports the gross amount the customer paid, not the net amount you actually received after fees. Many Indian businesses record only the net figure in their GST and income tax returns. The mismatch between the gross figure the platform reports and the net figure you declare is one of the most common triggers for an inquiry.

Permanent Establishment Exposure: Storing goods in an EU warehouse through an FBA-style arrangement creates a physical presence in that country. DAC7 reporting makes it easy for tax authorities to know exactly which warehouse holds your inventory. If you have stock in Poland but are not VAT-registered there, the DAC7 report from Amazon will flag this. The result is a “Failure to Register” notice from the Polish tax authority.

Reconciling Gross vs. Net Across Multiple Platforms: DAC7 requires platforms to report consideration net of fees charged by the platform. But different platforms calculate fees differently. A seller using Amazon, Etsy, and Upwork simultaneously will receive three settlement statements in three different formats, which all need to reconcile with a single GST return in India. This is not a theoretical problem. It is an active compliance gap for most Indian multi-platform sellers today.

The India-EU Trade Context

The timing of these directives is significant. The India-EU Free Trade Agreement negotiations concluded on 27 January 2026 at the 16th India-EU Summit in New Delhi. The deal, described by both sides as the “mother of all deals,” covers goods, services, investment, and digital trade. It is the largest trade agreement either party has ever concluded. However, as of this writing, the agreement still requires formal signing, legal vetting, translation into all EU languages, European Parliament consent, and EU Council approval before it enters into force. It has been concluded, not ratified.

What is already active, independent of the FTA, is the existing automatic exchange of information framework between India and EU member states under the OECDOrganisation for Economic Co-operation and Development. Its Common Reporting Standard (CRS) governs how countries automatically exchange financial data with each other every year. India participates in CRS, which is the existing channel through which DAC7 and DAC8 data from EU authorities reaches the CBDT.‘s Common Reporting Standard and bilateral tax information exchange agreements. DAC7 and DAC8 data flows into these existing channels. The GSTN is increasingly equipped to process incoming international data feeds, and the CBDTCentral Board of Direct Taxes. India’s income tax apex authority under the Ministry of Finance. It already receives foreign income disclosures from multiple countries through the OECD’s CRS framework and bilateral tax treaties. DAC7 and DAC8 data will flow through the same infrastructure. already receives foreign income disclosures through these frameworks. The FTA will deepen that cooperation further once it enters into force.

Building Your Defensive Core: Four Training Drills

The Tax Athlete does not wait for the match to begin before checking their gear. Here is how to build a compliance posture that can handle the triangulation scrutiny.

-

Synchronise Your Identity Data

Your legal name, PAN, and address on every EU-facing platform, Amazon, Upwork, Etsy, Airbnb, must be character-for-character identical to your Indian GST portal and ITR records. A mismatch in a single field (abbreviated name, outdated address) creates a data reconciliation failure on the EU side and delays or breaks the automatic exchange process.

-

Run Quarterly Settlement Reconciliations

Do not wait for year-end. Every quarter, pull your platform settlement reports and reconcile the gross consideration figure against your bank inward remittance statements. Any gap you catch internally is a gap you can explain. Any gap the EU system catches first is a gap you are already defending.

-

Audit Your Warehouse and Fulfilment Arrangements

If you are using FBA or any third-party logistics provider to hold inventory within the EU, get a clear legal opinion on your VAT registration obligations in each country where stock is stored. DAC7 reporting from Amazon will now tell German, Polish, or French authorities exactly where your goods are. Your VAT registrations need to match that picture.

-

Align Your HS Codes and Product Classifications

Your product codes must be consistent across your Indian GST returns, your EU customs declarations, your CBAM product filings (if you export steel, aluminium, cement, or fertilisers), and your platform listings. When the triangulation system runs, any classification inconsistency across these four data sources is a red flag. See the CBAM post for the specific HS code framework that matters for carbon-intensive exports.

Frequently Asked Questions

Conclusion: The End of the Honour System

In cricket, the Decision Review System (DRS) did not change the rules of the game. It changed who has the final word on what actually happened. DAC7 and DAC8 are the DRS of international tax. The rules that govern whether your income is taxable have not changed. What has changed is that the data to enforce those rules now arrives automatically, from multiple independent sources, before you file anything.

For Indian businesses with EU exposure, the window to self-correct is wide open right now. The data collection is live, but the full cross-referencing and enforcement machinery is still building. The Tax Athlete uses that window as a training period, not a rest period. Get your settlement data clean. Get your VAT registrations in order. Get your HS codes consistent. When the full system is operational, those who have done this work will find the European market as accessible as ever. Those who have not will find the automated inquiry already waiting.

The AI Audit Trap and Your Defensive Core

- How EU tax authorities use AI to assign a risk score to your business before an audit even starts

- The specific patterns in ViDA and CESOP data that trigger automated red flags

- How to use your own validation tools to audit yourself and fix errors before the government does it for you

- European Commission: Council Directive (EU) 2021/514 — DAC7

- European Commission: DAC8 — Crypto Asset Reporting Directive

- OECD: Model Reporting Rules for Digital Platforms — Sharing and Gig Economy (2020)

- EY Global: EU Adopts DAC8 — Tax Transparency Rules for Crypto Assets (October 2023)

- European Commission: EU-India Free Trade Agreement — Negotiations Concluded January 2026

- Ministry of Commerce and Industry, Government of India: India-EU FTA Fact Sheet (January 2026)

- Bloomberg Tax: Unpacking the EU’s DAC7 Directive